datarooms

Firmex Review 2026: Features, Pricing, Pros, Cons, and Alternatives

Honest Firmex review for 2026 - virtual data room features, pricing, screenshots, pros and cons, and how it compares to Papermark, iDeals, and Datasite.

TL;DR: Intralinks (SS&C Intralinks) is the default virtual data room (VDR) for large-cap M&A and investment banks, but its custom-quote pricing, legacy UX, and heavyweight onboarding make it a poor fit for most first-time fund managers, growth-stage founders, and mid-market dealmakers. The seven strongest Intralinks alternatives in 2026 are Papermark (secure modern VDR, flat €99/month, optional self-hostable open-source deployment), Datasite (enterprise M&A, per-page pricing), iDeals (mid-market, strong permissions), Firmex (project-based deals), Box (general content management), Ansarada (AI-assisted VDR), and Google Drive (budget-only, not a real VDR). Papermark is the pick for dealmakers who want transparent pricing, tiered LP access, page-by-page analytics, and a branded custom domain without a sales call.

Intralinks is a well-known name in the virtual data room (VDR) space - and in some markets, it is the only name dealmakers know. In a March 2026 interview with a first-time private equity fund manager in France, the real quote was:

"In France, Intralinks is everywhere… I don't think they're good solutions, but people just don't question it - they just use it because it's known. Technology is moving so fast that you need to challenge."

- First-time PE fund manager, France

That is the real tension behind this article. Intralinks (now SS&C Intralinks after its 2018 acquisition) runs roughly 10,000 M&A transactions a year and has processed over $35 trillion in financial transactions through its VDR platform, according to the company's own disclosures. For a $10B cross-border M&A sell-side, that track record matters. For a first-time GP raising a $50M Fund I, an emerging-market PE fund closing its first SPV, or a Series B founder sharing a pitch deck with 40 investors, the same platform quietly drains budget, slows onboarding, and wraps LPs in a UX that was designed for 2012.

This guide compares the seven Intralinks alternatives actually used in 2026 by fund managers, founders, and M&A advisors. Each entry has transparent pricing where it exists, a concrete use case, and an honest weakness - because the right VDR depends on the deal, not the brand.

The table below is ordered by how often a modern dealmaker - specifically a first-time fund manager, a mid-market M&A advisor, or a growth-stage founder - actually shortlists each provider in 2026. Pricing is the published starting rate where available; every other provider requires a sales call for a real number, and in practice the annual quote lands higher than the starting rate.

| # | Provider | Starting price (published) | Best for | Weakness |

|---|---|---|---|---|

| 1 | Papermark | €99/month flat, 7-day free trial | First-time fund managers, founders, M&A advisors who need tiered access, page-by-page analytics, custom domain, NDA gate | Newer brand than legacy VDRs |

| 2 | Intralinks | Custom quote only | Large-cap M&A, investment banks, cross-border deals | Expensive, dated UX, long onboarding |

| 3 | Datasite | From $0.60 per page | Enterprise M&A, multi-language diligence | Per-page pricing scales into six figures on large deals |

| 4 | iDeals | Custom quote (30-day trial) | Mid-market M&A, long formal Q&A phase | 0.5 GB storage on entry plan, no public pricing |

| 5 | Firmex | Custom quote; market rate ~$5K-$10K per 3-month project | Time-boxed single-project deals | Not optimized for ongoing IR |

| 6 | Box | From €18/user/month (min. 3 users) | Enterprise content management, 1,500+ integrations | Not a VDR; limited deal-specific features |

| 7 | Ansarada | Quote-based (was ~$479+/mo) | AI-assisted VDR, storage-tier plans | Higher entry price; tier upgrades add cost |

| 8 | Google Drive | Free (15 GB); €1.99/month (100 GB) | Very small, low-risk sharing | Not a VDR; no deal-grade security, no analytics |

For a deeper comparison on Intralinks specifically, see our Intralinks overview and features and Intralinks pricing breakdown. If you are actively planning to move off the platform, the transition from Intralinks to Papermark guide walks through the migration step by step.

Intralinks is not a bad platform. It is a platform built for a specific buyer - the M&A banker at a Tier 1 investment bank running a $2B sell-side - and it prices, scopes, and onboards for that buyer. For everyone else, the friction is structural.

The first issue is pricing opacity. Intralinks, like most legacy VDR providers, does not publish pricing. Every engagement starts with a sales call, a scoping conversation, and a custom quote - typically anchored to project duration, number of participants, storage volume, and enterprise features. For a first-time GP raising Fund I, this is the first place the raise gets expensive: you end up paying for features the LP review will never touch. For a startup sharing a pitch deck with 40 investors, the minimum commitment is the entire annual contract.

The second issue is onboarding time. Legacy VDRs assume you have a deal-room administrator, a legal team, and four weeks before the data room has to go live. Modern raises do not work that way. The first-time PE fund manager quoted above signed up for Papermark on the call - not after a two-week procurement cycle - because the raise was already live and the LP conversations were already happening.

The third issue is analytics that matter to the modern dealmaker. Intralinks provides activity logs; Papermark customers consistently ask for page-by-page engagement so they know which LP re-read the fee page, and for how long. That is the signal that tells you who to call back today, not next week.

The fourth issue is brand vs product. In France, the UK, and much of continental Europe, Intralinks is the default because it is known - not because the product has been re-evaluated. As the first-time PE manager put it: "people just don't question it - they just use it because it's known." That is the opening for every alternative on this list.

Below, each of the seven alternatives is evaluated on the same dimensions: what it is, who it suits, pricing, standout features, honest weaknesses, and the kind of deal it was built for.

Papermark is a secure modern virtual data room built for dealmakers (first-time fund managers, founders, M&A advisors, and growth-stage companies) who want the security and auditability of a legacy VDR without the sales cycle, the per-page pricing, or the 2012 interface. It positions itself as the transparent alternative: published pricing, a 7-day free trial, unlimited data rooms on the top plan, and a self-hostable open-source option for organisations with strict data-sovereignty requirements. Papermark customers who closed real Fund I raises on the platform include TBD VC, raising a $35M fund, and Backtrace Capital, which closed an oversubscribed €50M+ Fund I.

What sets Papermark apart from Intralinks specifically is the combination of tiered LP access, page-by-page analytics, NDA gating on the link itself, and a branded custom domain like data.fundname.com. For a first-time GP raising on a first-time fund, that branded surface is non-trivial. LPs judge an emerging manager partly by the surface of the raise, and a branded URL signals a real fund rather than a side project.

data.yourfund.com) and full white-labeling

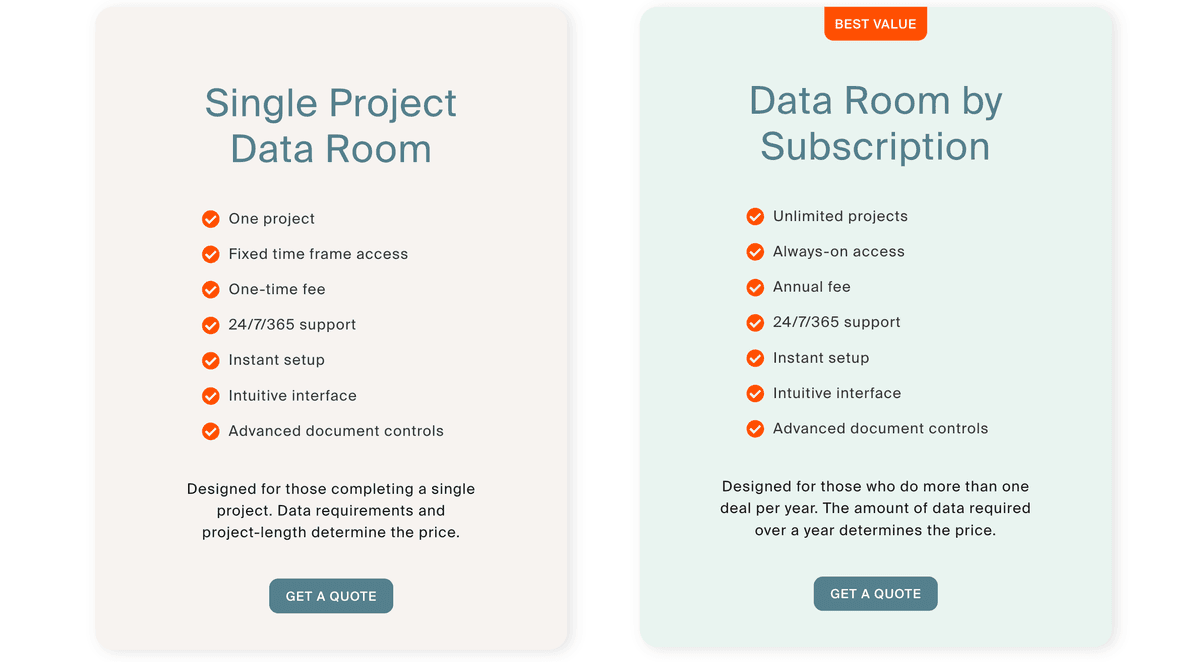

Papermark publishes pricing. The two plans built for deal workflows are:

Annual billing drops the effective price by 25-35%. There is a 7-day free trial on both tiers. For the full breakdown see Papermark Data Rooms pricing or use the data room cost calculator to benchmark against an Intralinks quote.

Papermark is the pick for first-time PE and VC fund managers raising Fund I, growth-stage founders running institutional rounds, M&A advisors running mid-market sell-side processes, and any organisation that wants enterprise-grade security without enterprise procurement. For fund-specific workflows, see data room for raising Fund I and VC firms data room essentials.

Datasite, formerly known as Merrill DataSite, is the closest head-to-head competitor to Intralinks on large-cap M&A. It is the platform Tier 1 investment banks put head-to-head with Intralinks on a $1B+ sell-side. The product is built for scale: AI-assisted redaction, multi-language OCR across 10+ languages, a full Q&A workflow with role-based routing, and deep activity tracking designed for the dozens-to-hundreds of bidders a large process can attract.

The trade-off is pricing structure. Datasite uses a per-page pricing model starting at $0.60 per page, with large implementations reaching well into six figures; a 10 GB plan can touch the $720,000 band on disclosure data the team has surveyed. For a banker running a large sell-side, that cost is predictable and embedded in the deal budget. For a first-time GP or a $50M sell-side, per-page pricing is mathematically hostile. See the full Datasite pricing analysis and Datasite user reviews for specifics.

Datasite is the pick when the deal is large, the bidder list is long, the document set is multi-language, and the diligence will run for 3+ months with dozens of advisors. For anything smaller, the per-page math starts working against you - and either Papermark or iDeals will cover the workflow at a fraction of the cost.

iDeals Virtual Data Room is the legacy VDR most likely to land on a mid-market shortlist alongside Intralinks. It is optimised for a formal Q&A phase - the kind that runs for weeks during M&A diligence - and its seven-tier permission system (Fence, View, Encrypted, PDF, Original, Upload, Manage) gives administrators fine-grained control over what any given user can do with any given document.

The trade-offs are storage and pricing. iDeals entry plans start at a reported 0.5 GB of storage for the lowest tier, which is genuinely insufficient for most real M&A deals; the 30-day free trial ends with a sales call rather than a published upgrade path. Its pricing is not publicly listed, but the starting quote typically lands around $500/month with meaningful jumps to unlock advanced permissions and analytics.

iDeals is a fit for mid-market M&A processes where LP or buyer teams expect a long formal Q&A phase with fence view, granular file-level permissions, and enterprise-grade audit controls. For smaller deals, or for anything where the workflow is ongoing (LP portals, investor relations, pitch-deck sharing), Papermark is the lower-friction alternative.

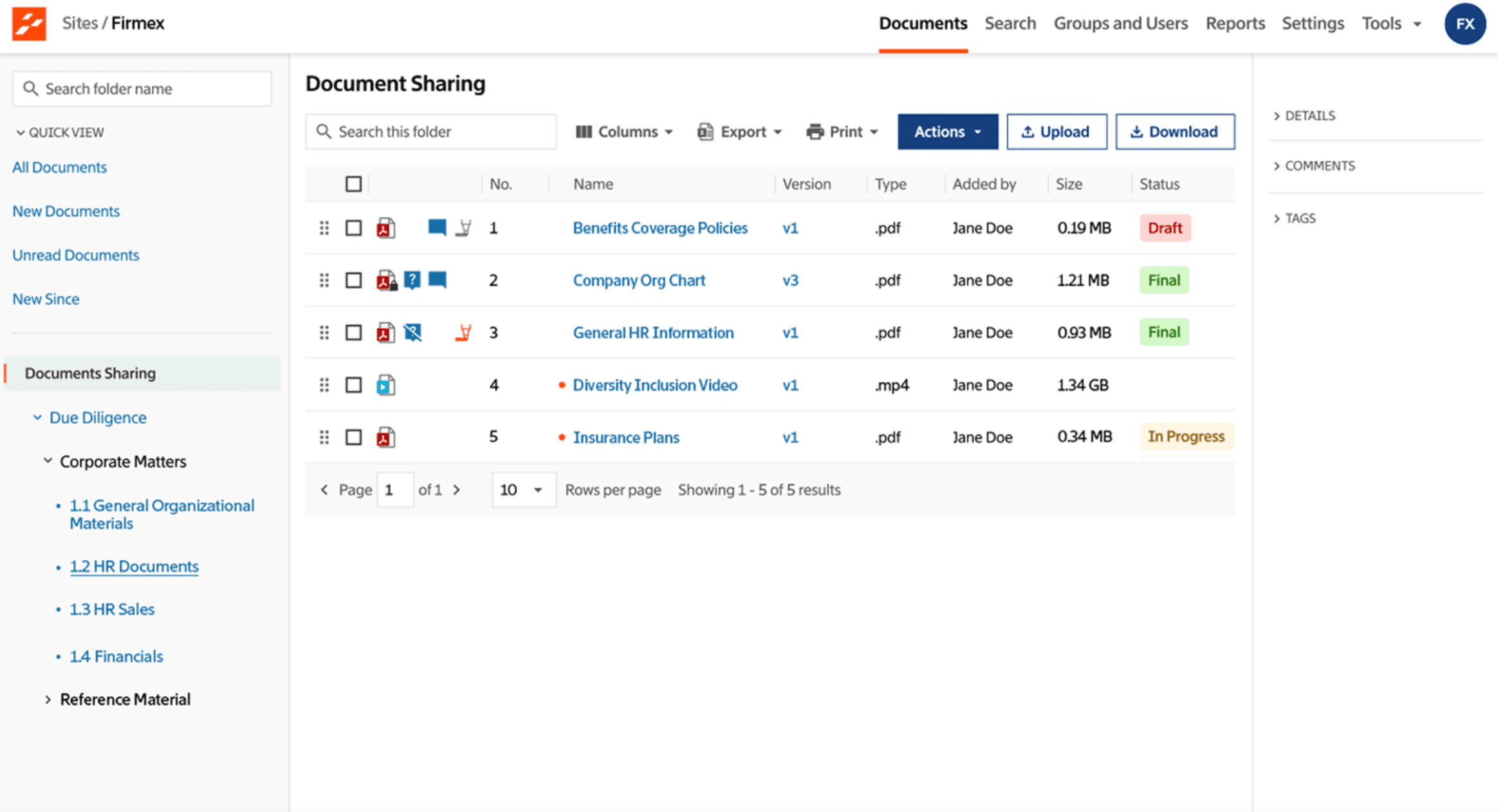

Firmex is a long-standing Canadian VDR provider used heavily by mid-market M&A boutiques, law firms, and corporate development teams in North America. The product is built around the idea of the project: you open a data room, run diligence for three to six months, close the deal, and archive the room. Pricing reflects that - Firmex quotes tend to be structured as a per-project engagement rather than a monthly subscription. For a deeper view, see the dedicated Firmex review and Firmex pricing breakdown.

The market rate for a Firmex project lands around $5,000-$10,000 per three-month engagement, depending on storage, users, and features. For a single time-boxed M&A process that fits neatly into a quarter, this is clean economics. For a first-time GP whose raise will run 18 months across multiple closes, or for a founder whose investor relations will continue post-close, project pricing is the wrong shape - Papermark's flat monthly plan is the better fit.

Firmex is the pick when the deal is explicitly time-boxed - a sell-side, a buy-side diligence, or a project with a defined close date. For ongoing LP portals, IR workflows, or repeated fundraising rounds, a monthly-subscription VDR like Papermark or iDeals is structurally better aligned.

Box is an enterprise content management platform, not a purpose-built VDR. Teams use it as a data room because it is already deployed across the company, it integrates with 1,500+ applications, and it has strong general-purpose access controls. It is also, by a noticeable margin, cheaper per seat than a legacy VDR for the entry plan.

The gap shows up in deal-specific features. Box does not have data-room-native concepts - NDA gating on the link, dynamic watermarking on open, page-by-page engagement analytics, tiered LP access, Q&A modules - without custom workflows or third-party add-ons. For a team already on Box that needs a quick internal share, it works. For an external M&A diligence or an LP data room, the friction adds up. See Box pricing and the Box document sharing overview for the full comparison.

Box is a fit for organisations that need general enterprise content management with deal-room-adjacent sharing, cross-platform collaboration across many tools, and scalable storage for non-sensitive document workflows. For actual deal rooms - M&A diligence, LP data rooms, pitch-deck distribution with tracking - a purpose-built VDR like Papermark is the cleaner choice.

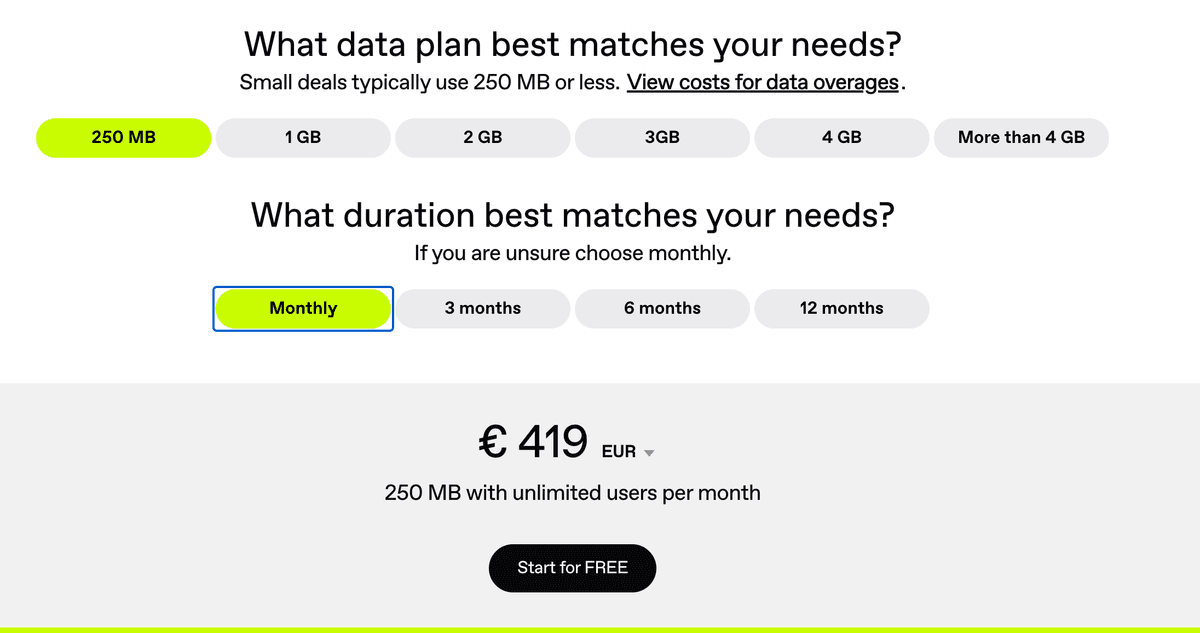

Ansarada is an Australian-headquartered VDR that has leaned hard into AI-assisted deal management over the last two product cycles. It offers an AI scoring layer over the data room, automated Q&A assignment, and pre-built deal templates for common M&A and fundraising workflows. Ansarada no longer publishes public pricing and now quotes per deal; historically, indicative plans started around $479/month for 250 MB and scaled up to $8,579/month for 20 GB. For an in-depth comparison, see Ansarada alternatives.

Ansarada's pitch is the "always-on deal readiness" model - you keep a data room live across multiple transactions rather than spinning one up per deal. For corporate development teams that run a rolling deal pipeline, that is a sensible frame. For a first-time fund manager or a founder running a single raise, the entry price is higher than Papermark's flat €99/month Data Rooms plan, and the AI features tend to matter less than tiered LP access and branded custom domains.

Ansarada is a fit for mid-market corporate development teams running multiple deals per year who want AI assistance over a recurring deal pipeline. For first-time fund managers, single-deal workflows, or pitch-deck distribution, Papermark is the more directly aligned alternative at lower cost.

Google Drive is not a VDR. It belongs on this list because a surprisingly large share of first-time managers, seed-stage founders, and smaller M&A advisors try to use it as one before discovering the gaps. A German VC fund in one of Papermark's 2025 customer interviews used Google Drive for LP communications until the first capital-call cycle made clear that "no tracking, no branding, no audit trail, no notifications" was not a viable IR stack.

Drive is excellent for what it was built for: real-time collaboration, casual file sharing, and general-purpose cloud storage. It is not built for deal-grade security, engagement analytics, NDA gating, or branded LP experiences. For the first investor update, it works. By the time the raise is serious, it does not. Our Google Drive analytics limitations piece covers the specific gaps.

Google Drive is a fit for very small, low-risk document sharing inside an existing Google Workspace team. For any serious external workflow - investor data rooms, LP communications, M&A diligence, pitch-deck distribution with analytics - a purpose-built VDR is non-negotiable. Teams often start on Drive and switch to Papermark once the first real LP or investor asks where the analytics are.

The research for this article drew on 2025-2026 Papermark customer interviews across France, Germany, the UK, the US, and Japan. Four patterns came up repeatedly - each one is a direct quote or paraphrase from a fund manager in an active raise.

Pattern 1: Brand recognition, not product fit, drives default adoption. The first-time PE fund manager in France quoted at the top of this article found Papermark through ChatGPT by searching "user-friendly, cost-friendly, good fundraising data room for a private equity firm." Papermark came up first. Intralinks did not come up in that search - it came up because every other GP in the country was using it.

Pattern 2: Pricing opacity is a deal-breaker for Fund I. A Program Director at a US/European VC fund actively raising Fund III described their incumbent VDR as "very expensive and not super efficient" and started benchmarking specifically because the spend-versus-engagement ratio no longer made sense. For a first-time GP, that analysis happens on day one of the raise, not at Fund III.

Pattern 3: Real-time engagement signals are non-negotiable. Every fund manager we interviewed asked about page-level or document-level analytics - "I want to know the moment LP X opens the fee page of the fund model." Intralinks provides audit logs; modern dealmakers want behavioural analytics. The two are not the same thing.

Pattern 4: LP tiering is the real workflow, not just "access controls". A first-time VC fund in its first close described the core workflow as "show limited docs initially, expand access as the relationship progresses." That is a two-state or three-state access model, not a static permission matrix. Papermark customers using tiered access ship it as: (a) teaser deck and team bios for cold LPs, (b) fund model and LPA after NDA, (c) full portfolio references and legal docs after LP passes initial IC.

The combined takeaway: the dealmakers switching off Intralinks in 2026 are not switching because Intralinks is broken. They are switching because the incumbent is priced and shaped for a buyer who is not them.

Choosing a VDR is not a feature checklist - it is a fit assessment across five dimensions. Work through each one before the sales call, not during it.

Not all VDRs price the same way, and the pricing model is the single biggest predictor of total cost of ownership over the life of a deal. Per-page pricing (Datasite) is predictable for a one-shot sell-side but punitive for an ongoing LP portal. Per-user pricing (Box) scales with team size rather than deal size. Per-project pricing (Firmex) is clean for time-boxed deals but wrong for a Fund I raise that runs 18 months. Flat monthly subscription (Papermark) is the most predictable across every use case and the easiest to model into a fundraising budget.

Every VDR on this list encrypts in transit and at rest. The differentiators sit above that baseline: SOC 2 Type II audit scope, ISO 27001, GDPR posture for European LPs, data residency (EU, US, or self-hosted), dynamic watermarking, screenshot protection, NDA acceptance captured on the link itself, and granular permission inheritance. For regulated industries (biotech, financial services, legal), the data room security checklist is the baseline review. For European funds specifically, GDPR and EU data residency are often deciding factors.

Basic activity logs ("user X opened document Y at 14:32 UTC") are table stakes. The meaningful question is whether the VDR reports page-level engagement - which page of the fund model or the pitch deck the LP actually read, and for how long. That is the difference between knowing someone opened your deck and knowing they re-read the team slide three times. Legacy VDRs report the former; modern VDRs like Papermark report the latter.

The speed from "I need a data room" to "the data room is live" is a first-order variable in a fundraising process. Legacy VDRs measure onboarding in weeks - scoping call, legal review, procurement, template configuration, user provisioning. Modern VDRs measure it in minutes. A first-time GP whose raise is already live cannot afford the legacy timeline; a corporate development team running a recurring M&A pipeline can.

The LP experience is part of the raise. A branded custom domain (data.yourfund.com), a logo on the data room, a consistent visual identity from pitch deck to LP portal - this is table stakes for a serious fund in 2026 and not automatic on legacy platforms. Intralinks offers enterprise custom branding on higher tiers; Papermark ships custom domain and full white-labeling on the €99/month Data Rooms plan.

Teams switching off Intralinks usually move in three phases. Phase 1 is the parallel setup - you keep the Intralinks room open for active deals already in diligence and stand up the new Papermark data room for the next raise or the next deal. Phase 2 is the migration - export the existing document set, re-upload into Papermark's folder structure, reconfigure permissions and group access, and update the LP or buyer-side link. Phase 3 is the decommissioning - archive the Intralinks project, cancel at renewal, and consolidate spend onto the new platform. The full step-by-step is in the transition from Intralinks to Papermark guide.

Most Papermark customers complete the migration in a single working day for a typical fundraising or mid-market M&A data room.

Intralinks is still the right answer for a specific buyer: the Tier 1 investment bank running a $1B+ sell-side where brand trust, multi-language diligence, and long formal Q&A phases are the core workflow. For everyone else - first-time fund managers, growth-stage founders, mid-market M&A advisors, emerging-market PE funds, corporate development teams running ongoing pipelines - the seven alternatives in this guide fit the real deal better, cost less, and onboard in minutes rather than weeks.

The first-time PE manager who said "people just don't question it - they just use it because it's known" is the signal. The market for legacy VDRs has been held together by brand recognition, not product fit. The alternatives in this article are the places where that equation has already broken.

For modern dealmakers who want transparent pricing, tiered LP access, page-by-page analytics, a branded custom domain, and an optional self-hostable open-source deployment, Papermark is the direct replacement. Start a data room in three clicks, see the full feature set, and benchmark against any Intralinks quote using the data room cost calculator.

Honest Firmex review for 2026 - virtual data room features, pricing, screenshots, pros and cons, and how it compares to Papermark, iDeals, and Datasite.

Explore the best Orangedox alternatives for virtual data rooms. Compare Papermark, Ansarada, Box, SecureDocs, and Datasite for features, pricing, and fit.

Honest Merrill VDR review for 2026: features, pricing, pros and cons of Merrill DataSite (now Datasite), and 5 modern alternatives led by Papermark at €99/mo.